As the name suggests, a Self Managed Superannuation Fund (SMSF) is one where the members are also the trustees and therefore have the freedom – and the responsibility – to make all of the decisions relating to the fund.

Some of these decisions include the fund’s investment strategy, the type of retirement planning strategies to undertake, the type of retirement income (pension) to use, the details of the trust deed for the fund, and so on.

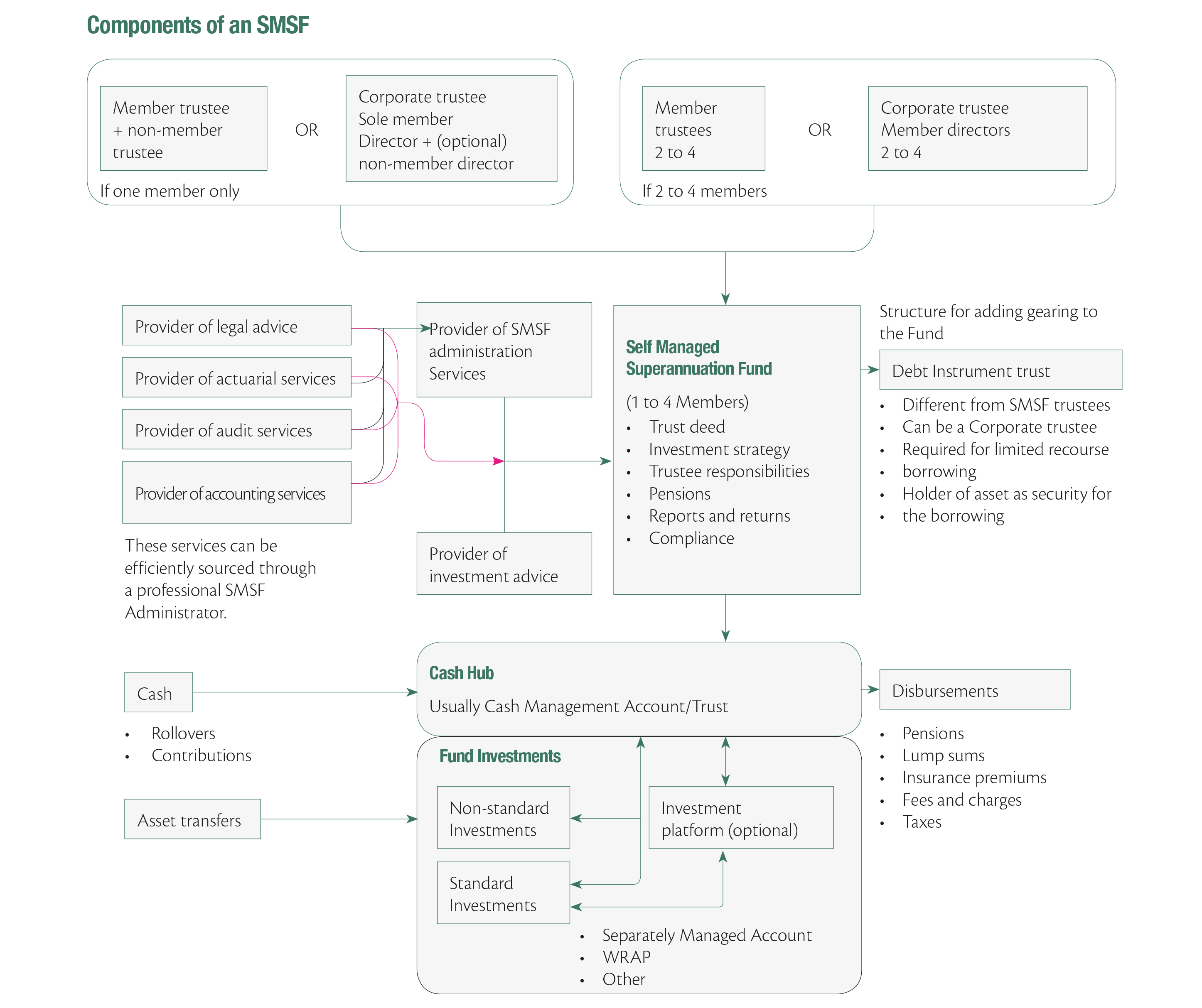

In order for any fund to operate efficiently and in accordance with superannuation and tax laws, the sourcing and coordination of various professional services is typically required. These services include accounting, auditing, financial planning, investment advice, legal advice and general administration.

What is the structure of a SMSF?

SMSFs can be quite simple or complex depending on the needs of the members.

As you can see, there are a number of aspects to consider when managing an SMSF. Trustees can choose to do a lot of this management themselves or, alternatively, they can engage professional service and product providers to minimise both the burden and the risk.

The first approach has the apparent advantage of minimising costs. However it can be time consuming and potentially risky if the trustees don’t have a strong knowledge of superannuation laws and requirements. It is worth bearing in mind that the penalties for breaching the law can be quite severe.

Engaging specialist service providers can remove a significant component of the management burden as well as greatly reducing the risk of breaching the law.

Typically a specialist SMSF Administrator will provide the transaction processing and accounting services and will source on behalf of the trustees the providers of legal, actuarial, and audit services as required.

Importantly, this allows the trustees to focus on the areas where they really want to have control, for example the investment strategy of the fund.

The following diagram illustrates the sorts of services and products that SMSFs typically employ.

Advice & assistance required

This structure needs to be supported by advice on all of the following points:

- Suitability of SMSF

- Set up of the SMSF

- Setting/adjusting the investment strategy

- Selecting and placing investments

- Estate planning

- Personal Risk Insurance

In order to provide advice and assistance on these major points the Trustee & Members need accurate & timely reporting once the Self Managed Superannuation Fund is in operation and that is when the selection of a capable SMSF Administrator becomes very important and how Gillespie Group SMSF Specialist can help you.

Gillespie Group SMSF Specialist service offering

Here’s a brief overview of the services and products that Gillespie Group offer to SMSF trustees to assist them in the successful management of their funds:

Administration service

SMSF administrators can support trustees by taking care of most of the administration requirements. Broadly, these include:

- Fund establishment including the provision of a trust deed, notice of election to become a regulated fund and registration for an Australian Business Number (ABN), Tax File Number (TFN) and Goods and Services Tax (GST)

- Compliance administration including providing annual financial and member statements, tax returns and all other necessary reporting to the ATO

- Independent audit facilitation

- Supplementary services including actuarial certification, calculation of lump sum and pension payments, and trust deed amendments

Cash hub

All SMSFs need a cash hub to enable them to manage their cashflow requirements such as the receipt of investment income and payment of fees and taxes.

SMSFs will typically use either a cash management account from a bank or a cash management trust from a financial institution.

These offer:

- Online access to facilitate easy reporting and transaction initiation

- The ability to give third parties such as the administrator or financial planner access to the account to initiate transactions such as fee or tax payments

- The ability to provide the trustee or administrator with data that enables them to meet the administrative and reporting

requirements of the fund - The ability to receive direct payment of investment income and facilitate the purchase of assets or the crediting of the proceeds from the sale of assets

- A high degree of security

Accounting

SMSFs can engage accountants to provide some aspects of the administration requirements including the preparation of financial statements, the preparation of the fund’s tax return, the payment of taxes and GST, and other general administrative duties. Alternatively, a specialist SMSF Administrator can supply these services.

Auditing

In addition, the fund must arrange an independent audit each year and must engage an auditor for this purpose.

Investments

There is a wide choice of investment options available for trustees to select from in order to meet the investment objective and strategy of their fund.

The most common types of investments are:

- Shares and other listed securities

- Separately managed accounts-where a share portfolio is constructed and managed for an investor in accordance with instructions from a professional investment manager

- Managed funds-covering most asset classes including Australian and international shares, property, alternative assets, fixed interest and cash

- Term deposits

- Direct property-including business real property, residential, commercial and retail property

- Collectables-for example artworks

Anne Steele – Accountant, SMSF Specialist Auditor and

registered Superannuation Auditor.

All of these investments can be owned directly by the fund on behalf of the members. However, it is also possible to simplify the management and administration of shares, managed funds, separately managed accounts and even term deposits through an investment platform such as a ‘wrap’ platform.

Holding investments through such a platform simplifies the management and administration of these assets while providing continuous online reporting plus consolidated annual tax statements.

Share brokerage

Some trustees prefer to manage their own share portfolio and will use a share broker to facilitate their share trading. This could be a full service broker or online share trading service.

Borrowing

An SMSF is able to borrow to invest by using a borrowing arrangement that meets the strict conditions under superannuation law. The actual investment can be anything that the fund can normally invest in, such as shares or property but the trustee must hold the investment through a separate, specialised trust commonly known as a Debt Instrument Trust (or bare trust) and the lender only has recourse to the assets that the trustee borrows against. There is no general recourse available to the lender against the fund itself.

The lender can be a bank, a margin lender, the SMSF trustee or a related party on commercial terms. It is important to set up this structure correctly to ensure that the arrangement is fully compliant with the law.

Legal and estate planning

Trustees may need legal services for various reasons, including the drafting of the trust deed of the fund.

Estate planning is also a very important area of retirement planning and is best done with specialist legal advice to ensure that the beneficiaries receive the desired level of benefits with the least amount of cost, tax and legal challenge.

Financial planning

Trustees may be confident in designing and implementing their investment strategy, however often they will employ the services of investment professionals to help in this area.

Financial planners can provide important advice to trustees, particularly in relation to:

- Retirement planning strategies that make the most of the tax and other advantages of the superannuation system and help fund members maximise their benefits

- Development, implementation and monitoring of the investment strategy of the fund

- Calculating the appropriate type and level of risk insurance

- Other matters such as a general compliance overview, advising the trustees of the implications of superannuation and tax rule changes and working with other service providers in the interests of the trustees

Insurance

SMSFs are able to own insurance plans on behalf of their members to protect them from the worst kind of unexpected events, such as serious injury, illness or death.

The insurance types most applicable to SMSFs are:

- Death – pays a lump sum if a member dies or is diagnosed with a terminal illness and has less than 12 months to live

- Total and Permanent Disablement (TPD)- pays a lump sum if a member can no longer work because they become totally and permanently disabled

- Income protection-pays a regular income while a member is totally disabled and is unable to work due to illness or injury or

partially disabled and, after returning to work, earns less due to illness or injury

How the Gillespie Group SMSF Service can help

The number of SMSFs registered in Australia has grown rapidly in recent years as more and more people are attracted to the benefits of managing their own fund.

If you are the trustee of an SMSF or are interested in setting up a SMSF, Gillespie Group is able to offer a number of products and services that can help. These include:

- Financial planning

- SMSF administration services

- Separately managed accounts

- Managed funds

- Investment platform

- Cash management account

- Term deposits

- Life insurance

- Facilitating the provision of other specialist services

Stuart Howard – Financial Planner and SMSF Specialist Advisor

Gillespie Group of SMSF Specialist Advisers

There are many providers that can give you advice but you would need to go to a few different businesses to get all the advice you need. Alternatively you can come to a one-stop-shop, such as the Gillespie Group, where the following team members can assist with all the requirements of your SMSF:

- John Gillespie – oversees the whole SMSF Service that we

provide. John is a Chartered Accountant, Certified Financial Planner,

Accredited Mortgage Consultant and registered Tax Agent. - Stuart Howard – Financial Planner and SMSF Specialist Advisor

after completing a course through Adelaide University. Stuart is a

member of the Financial Planning Association and holds a BA Hons

Economics degree. - Anne Steele – Accountant, SMSF Specialist Auditor and registered

Superannuation Auditor.

Collectively we have 50 years of experience in the establishment and ongoing management of SMSFs. To see if you can benefit from the extensive range of services we provide, we are happy to offer you a no cost initial meeting to discuss your new or existing SMSF in more detail. As an added incentive, should you decide to employ the Gillespie Group with respect to your fund before 30th September 2017, we are pleased to offer a 15% fee discount to new clients.

Gillespie Finance Directions Pty Ltd ABN 40 122 284 888

AFS and Australian Credit Licence No 478547

Phone 02 6260 4994

Fax 02 6260 4995

Level 1, 68-70 Dundas Court PHILLIP ACT 2606

PO BOX 6126 MAWSON ACT 2607

www.gillespiegroup.com.au